Economic Impact of Climate Change: A Alarming New Study

The economic impact of climate change is rapidly becoming one of the most pressing issues of our time, with new research suggesting that the economic toll could be six times worse than previously believed. As global temperatures continue to rise, many experts warn of dire consequences not just for our environment, but for economic stability and growth. In fact, macroeconomic analyses indicate that each increase of just 1°C could lead to a staggering 12% reduction in global GDP, underscoring the urgency of addressing this crisis. With extreme weather events becoming more frequent, the cost of climate change extends beyond immediate losses, threatening long-term productivity and spending. As we delve deeper into understanding these effects, it becomes clear that effective decarbonization policies are essential to mitigate risks and safeguard our economic future.

The financial ramifications of environmental change are becoming increasingly clear as economists reassess the potential consequences brought about by a warming planet. Known widely as the “cost of climate change,” this phenomenon reflects the myriad ways in which our economy could be adversely affected, from GDP reduction to increased spending on recovery efforts. As global temperatures continue to trend upward, researchers are exploring how such shifts can significantly disrupt productivity and economic growth on an unprecedented scale. Furthermore, the intricate relationship between climate and economic performance calls for robust decarbonization policies that can both stabilize economies and combat rising temperatures. Therefore, understanding these intersecting dynamics is vital to fostering a sustainable economic landscape moving forward.

Understanding the Economic Impact of Climate Change

The latest research underscores the profound economic impact of climate change, revealing that its toll may be significantly higher than once imagined. A startling conclusion from economists Adrien Bilal and Diego R. Känzig indicates that every increase of 1°C in global temperatures could directly equate to a 12% dip in global GDP. This alarming revelation suggests that the repercussions of climate change may be more immediate and severe than simply environmental degradation; rather, they have far-reaching implications for global economic stability.

As economies worldwide grapple with the ramifications of rising temperatures, the urgent need for comprehensive decarbonization policies becomes ever clearer. Past models underestimated the economic fallout, which has led to a critical reflection on how we project climate-related economic forecasts. In light of these findings, there is a pressing call for nations to reassess their strategies and invest decisively in sustainable practices to mitigate economic losses caused by climate impacts.

The Rising Costs Associated with Climate Change

The financial burden imposed by climate change is not only extensive but also growing rapidly. As researchers are finding that the economic toll—estimated to be six times greater than previous estimates—is directly linked to temperature fluctuations, businesses and governments alike are being compelled to reassess their climate adaptation strategies. The economic losses discourage consumer spending, reduce investment, and ultimately stifle economic growth, leading to a destabilized market. The rising costs associated with increasingly frequent extreme weather events further exacerbate this situation, presenting a dire need for immediate action.

Furthermore, the study highlights a significant disconnect between traditional economic growth models and the realities of climate change. While some economists have maintained a focus on ongoing productivity growth, the compounding effects of rising global temperatures present an increasingly untenable scenario. This underscores the importance of integrating climate risk into economic forecasting, ensuring that forecasts factor in the extensive costs of climate change, thus fostering a more resilient economic landscape that can withstand environmental upheavals.

Decarbonization and Its Economic Benefits

Amongst the daunting challenges posed by climate change, the concept of decarbonization emerges as both a solution and an economic opportunity. The latest figures suggest that the social cost of carbon requires reevaluation, highlighting decarbonization as a financially viable alternative for major economies. The research by Bilal and Känzig indicates that the benefits of implementing effective decarbonization policies easily outweigh the costs, establishing a strong foundation for sustainable economic policies aimed at reducing carbon emissions and mitigating climate impacts.

In addition to mitigating losses attributed to climate change, investing in decarbonization initiatives can stimulate job creation and foster technological advancements. By pivoting towards sustainable energy sources and reducing reliance on fossil fuels, economies could see an enhancement in productivity that promotes healthier long-term growth. As revealed in the study, decarbonization offers not just a pathway to environmental resilience but also the potential for substantial economic gain—essentially paving the way for future generations to thrive.

Climate Change and Global Economic Forecasts

As climate change continues to escalate, its implications for global economic forecasts become increasingly urgent. The revised mathematical models proposed by Bilal and Känzig highlight the necessity of integrating global temperature variances into future economic predictions. This methodological shift is aimed at providing a more accurate picture of how temperature fluctuations can spur economic downturns, particularly in developing nations that may be less equipped to handle these changes. Understanding this relationship between climate and economy is crucial for planning effective response strategies.

Moreover, the prospect of continued rising temperatures poses a unique challenge for fiscal planners and policymakers. Any reliable economic forecasting must now prioritize climate variables to mitigate significant future losses. As nations strive to predict economic growth in an era fraught with unpredictability, developing adaptive frameworks that center on climate resiliency becomes indispensable. Implementing such frameworks not only provides protection against the perils of climate impact but also sets a precedent for sustainable economic growth.

The Long-Lasting Effects of Climate Change on Economic Growth

The long-lasting effects of climate change on economic growth cannot be understated. Bilal and Känzig’s research suggests that if global temperatures rise by an additional 2°C, the global output and consumption could potentially reduce by half. Such a staggering forecast indicates that the threat of climate change transcends immediate environmental concerns, extending its reach into economic stability and growth. Historical analogs, such as the Great Depression, may pale in comparison to the ongoing economic turbulence posed by climate challenges.

These findings present a clarion call for nations to take preventive measures against the economic repercussions of climate change. Enhanced investment in renewable energy sources, green technologies, and sustainable practices must become a priority if societies wish to cushion themselves against the potential downturns forecasted. By doing so, we not only pave the way for healthier economic futures but also strengthen our global resilience against the inevitable effects of climate change.

Assessing the Social Costs of Carbon Emissions

Assessing the social costs of carbon emissions is integral to understanding the full economic implications of climate change. The dramatic difference between previous estimates of $185 per ton and the revised figure of $1,056 per ton underscores the urgency to recalibrate our approach toward environmental policy. Accurate assessments allow for a clearer understanding of how emissions directly influence economic output, highlighting the inherent need for robust climate frameworks that reflect these social costs.

Incorporating higher social cost estimates into national planning processes also enhances the accountability of businesses and governments in their environmental impacts. This shift aids in prompting investments in cleaner technologies while fostering public awareness regarding climate-related costs. By ensuring that policymakers factor the true social costs into their decision-making, society can create stronger incentives for adopting environmentally friendly practices, ultimately steering economies toward sustainable development.

Navigating Economic Adjustments Due to Climate Change

Navigating the economic adjustments due to climate change necessitates a multifaceted approach. As the study highlights, global temperature rises lead to increased instances of extreme weather, which in turn demand changes in infrastructure and resource allocation. Countries will face pressure to adapt economically, investing not only in immediate climate change mitigation strategies but also in long-term adaptation measures that prepare economies for the shifting climate landscape.

Such adjustments require collaboration among stakeholders at all levels, from local governments to multinational organizations. This collaborative spirit can drive innovative approaches to economic resilience, ensuring that investments are effectively targeted for maximum impact. The challenges presented by climate change should compel nations to forge stronger economic ties and share best practices, fostering a community that is better prepared for the economic impacts of climate-related events.

Climate Change’s Future Economic Implications for Developing Countries

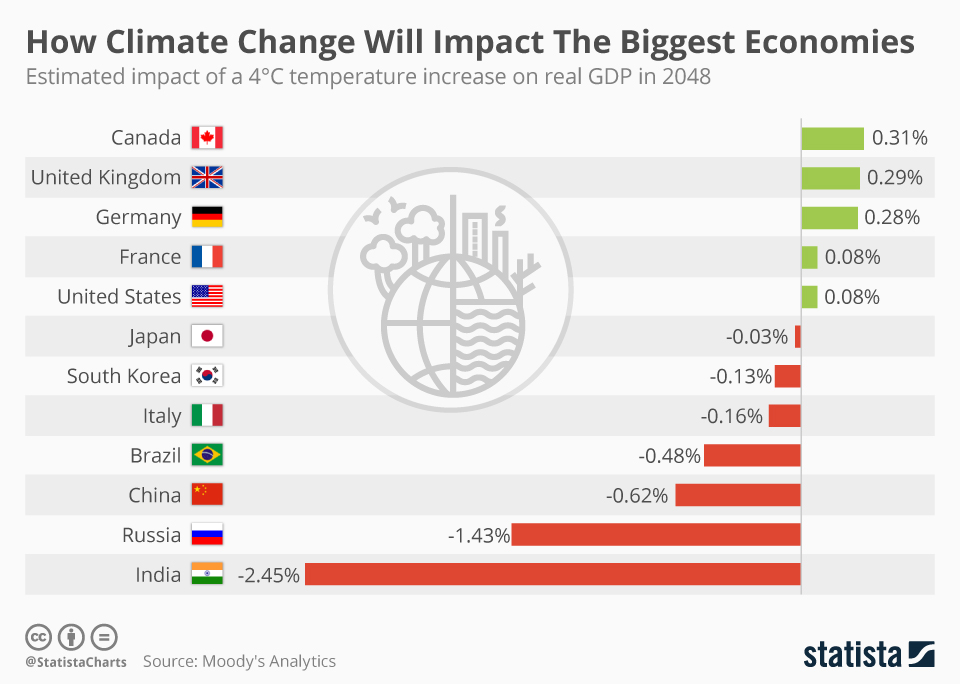

The future economic implications of climate change are particularly pronounced in developing countries, which often lack the infrastructure and resources to adapt quickly to environmental shifts. The findings of Bilal and Känzig suggest that such nations could suffer even more significant economic setbacks as globally rising temperatures correlate with deteriorating agricultural outputs, disrupted trade routes, and increased health crises. Without proactive measures, these economies are particularly vulnerable to the cascading effects of climate change.

Addressing climate impacts requires international support for developing nations, enabling them to build adaptive capacity and implement sustainable practices. By prioritizing equitable resource distribution and fostering global partnerships, the international community can better assist vulnerable economies in weathering the impending economic storms of climate change. Ensuring that all countries are prepared mitigates the potential for global economic instability fueled by inequality.

The Role of Policy in Combating Climate Change Costs

The role of policy in combating the costs of climate change cannot be overstated. With research indicating a significant jump in economic tolls linked to climate impacts, policymakers must prioritize frameworks that directly address these costs. Effective policies that incorporate rigorous climate action plans will not only work towards reducing emissions but also foster economic stability by reinforcing the connections between a healthy environment and a thriving economy.

Furthermore, the intersection of climate policy and economic strategy presents an invaluable opportunity for innovation. As countries pursue decarbonization, they can generate new industries and job opportunities that contribute to economic growth. By investing in renewable energy, sustainable agriculture, and green technology sectors, governments can create robust economies that are not only resilient to climate impacts but are also templates for how to harmoniously coexist with our planet.

Frequently Asked Questions

What is the economic toll of climate change on global GDP?

The economic toll of climate change is increasingly alarming, with recent studies indicating that every additional 1°C rise in global temperature can lead to a 12 percent reduction in global GDP. This suggests that the impacts of climate change are much more severe than previously estimated.

How does climate change impact economic productivity?

Climate change impacts economic productivity by causing a significant decline linked to rising global temperatures. With every additional degree increase, productivity can drop by 12 percent, posing a serious threat to future economic growth.

What are the estimated costs of climate change mitigation and their implications on the economy?

The estimated social cost of carbon due to climate change is approximately $1,056 per ton globally, which significantly exceeds earlier estimates. This higher cost emphasizes the economic benefits of implementing robust decarbonization policies that can mitigate the economic damage from climate change.

What does the research say about the long-term costs of climate change?

Research indicates that the long-term economic costs of climate change could lead to a 50 percent reduction in output and consumption if global temperatures increase by an additional 2°C. This loss surpasses the impacts experienced during the Great Depression, emphasizing the urgent need for effective climate action.

How does the decarbonization policy relate to the economic impact of climate change?

Decarbonization policy is crucial in addressing the economic impact of climate change. The recent findings suggest that the costs associated with decarbonization, estimated at about $95 per ton under the Inflation Reduction Act, are far lower than the economic toll of climate change, making a strong case for investment in sustainable practices.

What role does global temperature play in determining the cost of climate change?

Global temperature is a key factor in determining the cost of climate change as it correlates strongly with the frequency of extreme weather events, which devastate economic output. A rising global temperature has been found to significantly enhance the economic damages faced by countries.

Can we expect economic growth in a warming world?

While it is possible that economic growth may continue despite rising global temperatures, the growth will be significantly hindered. Predictions suggest that by 2100, the economy could be twice as wealthy without the impacts of climate change, highlighting the severe economic slowdown caused by increasing temperatures.

How has the understanding of climate change’s economic impact changed recently?

Recent research has shifted the understanding of climate change’s economic impact, revealing that previous estimates may understate the economic toll. New methodologies have shown that the damages to GDP could be six times greater than earlier assessments, emphasizing the critical need for updated economic models.

What can be inferred from the relationship between technological advancements and climate change?

While technological advancements can drive economic growth, they often contribute to emissions, exacerbating climate change. This complex relationship means that economic growth must be managed carefully to mitigate the long-term economic impacts of climate change.

How does extreme weather contribute to the economic cost of climate change?

Extreme weather, which is increasingly resulting from rising global temperatures, leads to significant economic damage by disrupting productivity and damaging infrastructure. The correlation between global temperatures and extreme weather events highlights the urgent need for strategies to mitigate these economic impacts.

| Key Points | Details |

|---|---|

| Economic Toll of Climate Change | New studies indicate the economic impact may be six times greater than earlier estimates. |

| Global Temperature Rise | Each 1°C rise in temperature could cause a 12% reduction in global GDP. |

| Long-term Impacts | A further 2°C increase by 2100 could reduce output and consumption by 50%, equivalent to double the impact of the Great Depression. |

| Methodology | Utilized global temperature as a primary factor to analyze economic impacts across 173 countries. |

| Social Cost of Carbon | Estimated social cost of carbon is $1,056 per ton, showing the necessity for decarbonization policies. |

| Decarbonization Benefits | Decarbonization shows favorable cost-benefit for major economies such as the U.S. and EU. |

Summary

The economic impact of climate change presents unprecedented challenges, highlighting that the financial toll will be significantly greater than previously assumed, potentially leading to a 12% reduction in global GDP per degree of warming. This underscores the urgency for robust climate action and adaptation strategies, as the long-term consequences of inaction could result in devastating economic losses, echoing past economic crises yet on a much larger scale. Thus, addressing climate change is not merely an environmental imperative but a necessary economic strategy.