Corporate Tax Reform: Examining the 2017 Tax Cuts Impact

Corporate tax reform has become a pivotal topic of discussion, especially as lawmakers analyze the ramifications of the Tax Cuts and Jobs Act (TCJA), enacted in 2017. As key provisions of this legislation approach expiration in 2025, debates grow more heated regarding whether to raise corporate tax rates or to extend tax cuts that are believed to spur investment growth and economic activity. Critics argue that halting or reversing the corporate tax cuts could impede economic recovery, while proponents of higher rates argue that it’s crucial for generating necessary revenue for other public initiatives, such as the Child Tax Credit. Studies indicate that while corporate tax cuts were intended to drive investment and benefit workers, the actual economic impact of these tax policies is complex and varies widely. Ultimately, the outcome of this ongoing discussion will significantly shape the economic landscape and corporate tax strategies in the United States.

The discussion surrounding corporate tax modification has garnered increased scrutiny in recent years, particularly in light of the implications of the 2017 fiscal reform legislation. As important aspects of this tax overhaul, popularly known as the Tax Cuts and Jobs Act, set to expire soon, the nation faces a critical juncture on whether to increase corporate tax obligations or extend existing reductions designed to stimulate business investment. Advocates for raising corporate tax rates highlight the necessity of reform as a means to boost government revenue and support social programs, including direct assistance to families through measures like the Child Tax Credit. On the other hand, proponents of maintaining lower rates argue that such policies are essential for fostering economic growth and facilitating investment. The forthcoming debates will undoubtedly influence the trajectory of both corporate finance practices and broader economic health.

Assessing the Legacy of the Tax Cuts and Jobs Act

The Tax Cuts and Jobs Act of 2017 marked a pivotal moment in U.S. tax policy, significantly altering corporate tax rates and providing substantial incentives aimed at stimulating economic growth. However, as we approach the expiration of various provisions of the TCJA in 2025, it becomes crucial to assess its long-term impacts. Economists and policymakers are divided on whether these tax cuts successfully delivered on their promise of driving robust business investment and economic prosperity. A careful analysis of the available data reveals a more nuanced narrative, suggesting that while reductions in corporate tax rates were intended to encourage growth, the actual outcomes were not universally favorable.

Critics argue that the TCJA primarily benefited large corporations without equating to corresponding increases in wages for workers or significant investment in communities. A study conducted by Harvard macroeconomist Gabriel Chodorow-Reich and his colleagues provides empirical insights into these claims. Their findings indicate that while corporate investments rose modestly, the fiscal consequences of the law have been stark, leading to a dramatic decline in federal corporate tax revenue. This raises questions about the effectiveness of the law in balancing corporate interests with broader economic benefits.

Corporate Tax Reform: The Future of Tax Policy

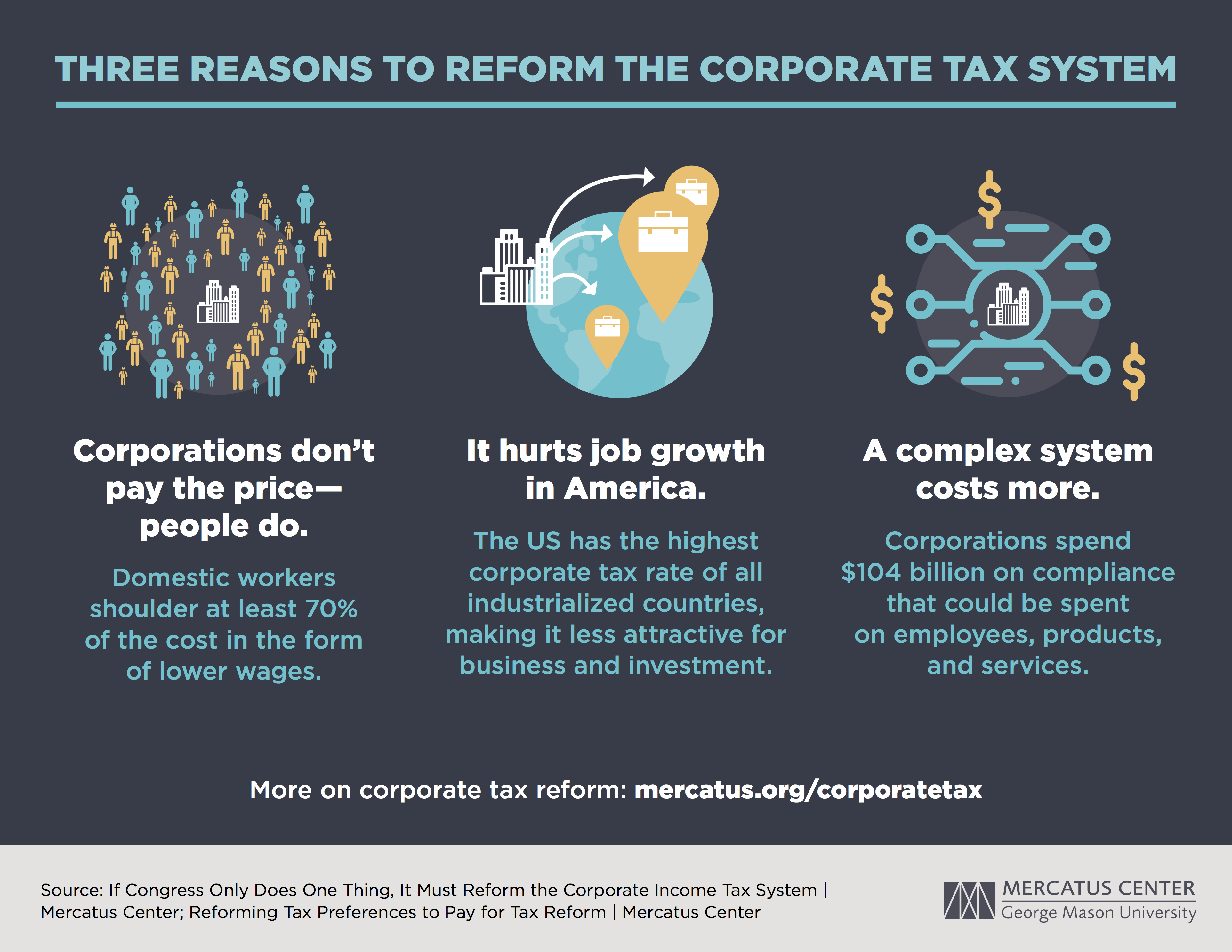

As discussions around corporate tax reform intensify, it is crucial to consider the implications of raising corporate tax rates. Current debates are polarized, with notable figures advocating for both a return to higher tax rates and the continuation of the existing cuts. While proponents of raising rates claim it will provide necessary funding for public services and economic initiatives, opponents highlight the potential negative impacts on business investment and job creation. The challenge lies in finding a balance that encourages corporate growth while ensuring that governmental needs are met through adequate revenue.

In analyzing the potential benefits of corporate tax reform, it becomes evident that the conversation must also include provisions such as the Child Tax Credit and incentivizing investment growth through targeted measures. Reforming the corporate tax landscape requires a comprehensive understanding of the economic impact of tax policy. By selectively adjusting the corporate tax framework, legislators can maximize opportunities for investment while alleviating the burden on middle-class families, highlighting the significance of integrating both corporate tax reform and household tax adjustments in future legislation.

The Economic Impact of Corporate Tax Rates

Corporate tax rates play a critical role in shaping the investment landscape within an economy. Reductions in these rates, as seen in the TCJA, were aimed at fostering a business-friendly environment, but the actual economic impact has been a topic of extensive debate. Research indicates that while lower rates may encourage some forms of investment, they do not universally lead to increased wages or broader economic benefits. Adjusting corporate tax rates must be part of a multifaceted approach that considers the interplay between taxation and economic productivity.

Furthermore, the reactions from businesses following tax rate adjustments can vary significantly. Some sectors may thrive under reduced corporate tax burdens, leading to increased capital investments, while others may not respond as favorably. As argued by Chodorow-Reich and his co-authors, focusing on targeted tax measures that promote specific investment activities, such as those related to research and development, might yield more positive outcomes than sweeping rate cuts. Understanding these dynamics is essential for policymakers seeking to implement effective reforms that stimulate economic growth.

Impact of Child Tax Credit on Economic Equity

The Child Tax Credit (CTC) has emerged as a significant tool in addressing economic inequality in the United States. As part of the TCJA, its expansion provided critical support to families, making it a central issue in the ongoing debate about tax reform. However, with the impending expiration of the more generous provisions of the CTC, there are growing concerns about the potential regression in economic equity that may follow. Advocates argue that maintaining and enhancing the CTC is essential for supporting low- and middle-income households, which ultimately fosters a more equitable economy.

As the discussions about tax reform evolve, the CTC’s role cannot be overlooked. Its effectiveness in lifting families out of poverty and providing economic stability hints at the broader implications of tax policy on societal wellbeing. Failing to renew the expanded Child Tax Credit not only threatens to reverse progress made towards economic equity but also undermines the potential multiplier effects that consumer spending from these families could have on the economy. Therefore, any corporate tax reform must consider the implications on household tax benefits, ensuring a balanced and inclusive approach.

Restoring Investment Growth Through Targeted Tax Measures

The link between corporate tax policy and investment growth is a focal point in economic discussions surrounding the TCJA. While proponents of the law argued that lowering corporate tax rates would drive significant capital investment, the actual outcomes suggest a more moderate increase in investment levels. Insights from Chodorow-Reich’s analysis highlight that expiring provisions specifically designed for encouraging capital investments led to more substantial gains compared to generalized rate cuts. This suggests that a more targeted approach to tax measures could be more effective in stimulating investment.

To drive sustainable investment growth, lawmakers should prioritize policies that directly incentivize innovation and capital expenditures. Reviving provisions that allow for immediate expensing of capital investments and supporting research initiatives could provide a clearer pathway for firms looking to expand their operations. By anchoring tax reform in strategies that focus on nurturing growth through targeted measures rather than blanket reductions, policymakers can create a framework that effectively fosters long-term economic prosperity.

Understanding the Political Landscape of Tax Reform

The political landscape surrounding tax reform is rife with contention, especially as we near the expiration of the TCJA provisions. With the potential for corporate tax increases on one side and calls for further reductions on the other, the debate raises fundamental questions about fiscal responsibility and economic strategy. Lawmakers from both parties are leveraging these issues in their campaigns, making the 2025 imposition of renewal or reform a pivotal electoral discussion. Understanding these dynamics is crucial for deciphering how tax policy may evolve in the near future.

Moreover, public sentiment towards tax reform is influenced heavily by perceptions of fairness and efficacy. Voters increasingly expect tax policies to promote not just corporate success but also wider societal benefits, advocating for solutions that harmonize the interests of businesses with the economic needs of individuals and families. As such, successful tax reform will likely hinge on an ability to strike a balance that resonates with constituents while also addressing the fiscal needs of the government, showcasing the interconnectedness of tax policy with everyday economic realities.

Corporate Tax and Global Economic Competitiveness

In a competitive global market, corporate tax rates are a significant factor influencing multinational corporations’ decision-making processes regarding where to allocate resources and investments. Since the TCJA, the U.S. has maintained a relatively favorable corporate tax rate compared to other nations, leading to discussions about the need for ongoing reform. It is essential for American corporations to remain attractive to investors while ensuring that the tax structure supports domestic economic interests and innovation.

Reassessing corporate tax rates in light of global trends is critical for ensuring that the U.S. maintains its competitive edge. However, simply cutting rates is insufficient; reforms should also consider potential impacts on investment behavior, domestic job creation, and overall economic growth. Enhancing incentives related to research and development investments and focusing on accumulated capital can help align U.S. tax policy with the realities of the global economy, promoting a sustainable environment for corporate activities while optimizing tax revenue.

Navigating the Future of Economic Policies and Taxation

As the expiration of significant components of the TCJA looms on the horizon, navigating the future landscape of economic policies and taxation becomes increasingly complex. Recognizing the interdependencies between corporate tax reform, household tax benefits, and overall economic health is vital for formulating effective policy. In the face of substantial pressures from various stakeholders, from corporate lobbyists to social advocates, achieving a consensus on tax reform will require careful consideration and compromise.

Looking ahead, policymakers must strive to create a taxation framework that reflects shared values and priorities of the society. This involves not only revisiting existing tax provisions but also embracing more comprehensive reforms that can generate sustainable revenue while promoting economic growth. Engaging with economists, businesses, and the public will be crucial in developing a tax system that addresses current challenges while laying the groundwork for long-term prosperity and fairness.

Frequently Asked Questions

What is Corporate Tax Reform and how does it relate to the Tax Cuts and Jobs Act?

Corporate Tax Reform refers to changes made to the way corporations are taxed. The Tax Cuts and Jobs Act (TCJA), enacted in December 2017, is one of the most significant reforms in recent history. It reduced the corporate tax rate from 35% to 21%, aiming to increase investment and economic growth by making U.S. corporations more competitive globally.

What was the economic impact of the Tax Cuts and Jobs Act on corporate investment?

The economic impact of the Tax Cuts and Jobs Act was a modest increase in corporate investment. According to analyses, capital investments rose by about 11% following the TCJA. However, these gains were not sufficient to offset the significant decline in corporate tax revenue, which dropped by 40% immediately after implementation.

How did the corporate tax rate changes under the TCJA affect wages?

The changes to corporate tax rates under the TCJA were predicted to drive up wages significantly, with estimates suggesting increases of $4,000 to $9,000 per employee. However, research indicates that actual wage increases were closer to $750 per year, suggesting the law’s effects on wages were more modest than proponents expected.

What key provisions of the TCJA aimed to encourage investment growth?

Key provisions of the TCJA that aimed to encourage investment growth included the ability for firms to immediately write off the entire cost of new capital investments and research expenditures. These expensing provisions were found to be more effective at stimulating investment compared to broad statutory tax rate cuts.

What does the debate over Corporate Tax Reform indicate about future fiscal policy?

The debate over Corporate Tax Reform highlights the conflicting views on fiscal policy among politicians. While Democrats advocate for raising corporate tax rates to fund social programs, Republicans argue for further cuts to promote economic growth. This ongoing discourse will significantly shape future tax legislation and its implications for economic policy.

How does the expiration of certain Tax Cuts and Jobs Act provisions affect households?

Several provisions from the Tax Cuts and Jobs Act are set to expire by the end of 2025, including expanded benefits like the Child Tax Credit aimed at households. The expiration of these provisions raises concerns among voters, as they could lead to increased tax burdens for families if not renewed.

Why are corporate tax revenues expected to change as TCJA provisions expire?

Corporate tax revenues are expected to fluctuate as TCJA provisions expire. With the expiration of expensing provisions aimed at driving investment growth, there is a potential for a dip in corporate investments. Additionally, the reinstatement of higher corporate tax rates could deter some business activity, further influencing revenue patterns in the future.

What role does the Child Tax Credit play in the discussion of Corporate Tax Reform?

The Child Tax Credit is a critical component of discussions around Corporate Tax Reform, particularly as it relates to funding and economic equity. As provisions expire, the balance between individual tax benefits and corporate tax rates becomes a focal point in debates about fiscal responsibility and the prioritization of tax relief for families versus corporations.

| Key Points |

|---|

| Corporate Tax Debate: There is a contentious debate over raising or cutting corporate tax rates as the TCJA provisions are set to expire in 2025. |

| Impact of TCJA: A Harvard study indicates that while there was a modest increase in wages and investments, the tax cuts did not pay for themselves and resulted in significant revenue loss. |

| Expired Provisions: Some of the most effective provisions were those related to immediate capital expensing, which outperformed simple rate cuts. |

| Corporate Tax Revenue: Following an initial drop, corporate tax revenue rebounded significantly due to soaring business profits, raising questions about the long-term effects of the TCJA. |

| Future Recommendations: Experts suggest re-evaluating the corporate tax structure, potentially raising rates while restoring beneficial expensing provisions. |

Summary

Corporate Tax Reform is an essential topic in the current economic climate as Congress prepares for potentially significant tax revisions in 2025. The analysis of the Tax Cuts and Jobs Act (TCJA) reveals critical insights into its impacts, revenue ramifications, and the effectiveness of various provisions. With ongoing debates about balancing tax rates and fostering economic growth, understanding these nuances will be pivotal in shaping the future of corporate taxation in the United States.