Commercial Real Estate Crisis: Economic Impact in 2024

The commercial real estate crisis has emerged as a pressing issue in today’s economic landscape, drawing attention from financial experts and investors alike. With high office vacancy rates escalating in major U.S. cities, the ramifications extend beyond just diminished property values; they pose significant risks to the broader economy. The regional banking sector, heavily laden with commercial real estate loans approaching maturity, faces mounting stress that could result in adverse economic impacts if a wave of defaults materializes. As vacancies remain stubbornly high and interest rates continue to rise, the potential fallout threatens the stability of financial institutions and their ability to lend. Observers warn that without proactive measures and regulatory interventions, the ripple effects of this crisis could be felt across various sectors, challenging the resilience of the current economic recovery.

The current turmoil in the commercial property market is raising alarms about the stability of the financial landscape, with many foreseeing a significant downturn. As businesses adapt post-pandemic, the rising rates of unused office spaces contribute to fears of a burgeoning crisis in the property market. This situation not only threatens the value of real estate investments but could also destabilize smaller financial institutions that are heavily exposed to these assets. The interplay between increasing vacancy levels and banking sector vulnerabilities poses critical questions about the future of lending practices and economic health. In this complex environment, the intricate web of financial regulation and investment strategies will determine how effectively these challenges can be navigated.

The Current State of Office Vacancy Rates

In the wake of the pandemic, many cities are facing alarmingly high office vacancy rates, ranging from 12 to 23 percent in major urban areas like Boston. This trend has come as a shock to the commercial real estate market, which previously thrived on the demand for office spaces. As companies adopt more flexible work arrangements, the traditional model of workplace occupancy faces unprecedented challenges. The subsequent decrease in demand has led to a significant depreciation in property values, prompting concerns within the economic landscape.

The high office vacancy rates not only reflect changing societal norms in work and communication but also point toward broader economic implications. With commercial real estate playing a pivotal role in local economies, prolonged vacancy can lead to reduced tax revenues and, by extension, diminished city services. Economists warn that if the trend continues, neglected commercial spaces could morph into urban blight, ultimately affecting regional growth and opportunities for potential businesses.

Commercial Real Estate Crisis: Causes and Consequences

The looming commercial real estate crisis can be traced back to a combination of factors, primarily the over-leveraging of properties during a period of low interest rates. Investors, buoyed by apparently stable conditions, took on substantial debt, leaving them unprepared for the reality of rising rates that followed. This precarious situation is intensified by the pandemic’s lasting impact, which has altered demand dynamics in office spaces significantly.

As commercial loans become due en masse, the potential for widespread delinquencies raises alarms among economists and financial experts. If these debts turn sour, the rippling effects could extend beyond the real estate sector, adversely affecting the regional banking sector. The resultant pressures threaten job stability and economic growth, casting a shadow over the financial landscape as stakeholders brace for significant repercussions from the unfolding crisis.

Financial Regulation and Its Role in the Current Crisis

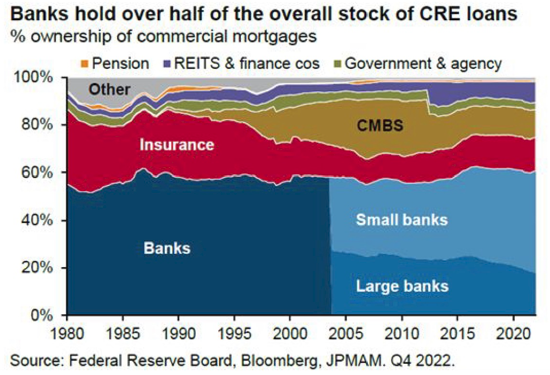

In light of the evolving commercial real estate crisis, the role of financial regulation remains paramount. Since the 2008 financial meltdown, stricter regulations were put in place to shield large banks from potential catastrophic failures stemming from bad real estate loans. These regulations have allowed major institutions to better withstand the kind of downturn currently facing the real estate sector. However, smaller banks, often subject to lighter regulatory scrutiny, may find themselves more vulnerable as the crisis unfolds.

As regional banks grapple with the ramifications of high office vacancy rates and plunging property values, the regulatory framework will be closely examined. Investors and regulators alike are anxious to see if the existing safeguards are robust enough to protect against a wave of commercial delinquency, which could lead to forced consolidations or bank failures. The current situation showcases the delicate balance needed to ensure stability within the banking sector, presenting a critical challenge for policymakers.

Economic Impact of High Office Vacancy Rates

The economic repercussions of high office vacancy rates extend far beyond the commercial property market, seeping into various facets of the economy. With a significant portion of office spaces remaining vacant, local economies experience a downturn in business activity, leading to reduced consumer spending and job losses in industries reliant on office workers. This scenario portends a more considerable strain on regional banks, which have backed many of these commercial properties.

Moreover, as economic conditions deteriorate, lower office occupancy translates to decreased sales for local retailers catering to office workers. The cumulative impact exacerbates challenges for cities—leading to potential cuts in vital services or investments in community projects. Therefore, ongoing monitoring of office vacancy rates becomes imperative not only for real estate stakeholders but also for economic planners focused on sustaining growth at a local level.

Regional Banking Sector at Risk: An Overview

With the commercial real estate sector under threat, the regional banking sector stands particularly at risk due to its heavy entanglement with real estate loans. Many smaller banks have concentrated their portfolios on commercial properties, making their financial health increasingly precarious as loan maturities approach. The failure of even a few regional banks due to delinquent loans could trigger broader financial instability.

Regional banks are further strained by rising interest rates, which have drastically affected the asset values of long-term loans. If these banks begin to encounter significant losses from their commercial real estate investments, the impacts could lead to stricter lending conditions, adversely affecting consumers and local economies alike. This makes the analysis of the regional banking sector’s health a matter of pressing concern as the commercial real estate crisis unfolds.

The Future of Commercial Real Estate: Opportunities Amidst Challenges

Despite the challenges posed by high office vacancy rates and the risks associated with commercial loans, opportunities may still arise within the real estate landscape. For instance, property owners may consider repurposing unused office spaces into residential or mixed-use developments, aligning with current housing shortages in urban areas. Such transitions could unravel new economic prospects and potentially moderate the impacts of the ongoing crisis.

Moreover, organizations that focus on adapting to evolving workplace needs, such as flexible office spaces or shared work environments, may find success in the changing landscape. By investing in properties that cater to modern work arrangements, these businesses could revitalize segments of the commercial real estate market that are currently struggling. Thus, the silver lining amidst the crisis could be characterized by innovation and adaptability among investors and entrepreneurs.

Assessing the Long-Term Outlook: Can Recovery Happen?

While the current commercial real estate crisis presents numerous hurdles, the long-term outlook remains cautiously optimistic. An eventual shift in market dynamics, driven by the necessity for adaptive reuse of properties and the gradual recovery of the economy, could foster a resurgence in office occupancy rates over time. Investors displaying patience and strategic foresight may benefit from acquiring undervalued properties ahead of a market rebound.

Efforts to stimulate economic growth, such as potential policy adjustments by financial regulators, could also play a role in moderating the crisis’s impacts. By addressing the issues posed by high office vacancy rates and supporting the regional banking sector, a foundation for robust recovery can be established. The key remains in navigating through adversity to uncover opportunities for sustainable growth in the commercial real estate sector.

The Importance of Monitoring Financial Regulations

The evolving commercial real estate crisis underscores the necessity of vigilant monitoring of financial regulations. As regulators assess the current economic landscape, they must ensure that safeguards for the banking sector remain effective while adapting to emerging challenges posed by high office vacancy rates and delinquent commercial loans. Ensuring a robust regulatory framework will be critical in navigating potential sector pitfalls.

Simultaneously, maintaining open lines of communication among industry stakeholders, regulators, and financial institutions will pave the way for collaborative solutions to the crisis. Continuous dialogue could result in informed policy adjustments that bolster both consumer confidence and market stability, helping to mitigate risks in a volatile economic environment.

Addressing Delinquent Loans in the Real Estate Sector

Delinquent loans within the commercial real estate sector can create a significant ripple effect on the wider financial system. As regional banks struggle with potential defaults, it becomes crucial to formulate proactive strategies that could safeguard their health. This may involve leveraging financial innovations or restructuring debts that allow banks to better manage their loan portfolios.

Furthermore, addressing the issue of delinquent loans should extend to supporting property owners in maintaining solvency through tailored refinancing options or financial assistance programs. Facilitating timely interventions could lead to the preservation of properties and the stabilizing of the regional banking sector, ultimately shielding the broader economy from the worst impacts of the crisis.

Consumer Impact: Balancing Risks and Rewards

As the current commercial real estate crisis unfolds, its implications reach consumers who may face heightened challenges relating to lending access and economic stability. Stricter lending criteria from regional banks struggling with their balance sheets could impact consumer credit availability, making it harder for individuals and businesses to secure loans. This tightening of credit could slow down the local economy as spending contracts.

However, amidst these challenges, some consumers may experience benefits. For instance, an oversupply of office space could eventually lead to lower rental prices, creating opportunities for startups or businesses seeking affordable operational spaces. Thus, while the crisis poses significant risks, it also presents potential rewards that savvy consumers and entrepreneurs may seek to capitalize upon.

Frequently Asked Questions

What is the current state of office vacancy rates in relation to the commercial real estate crisis?

Office vacancy rates have surged since the pandemic, now ranging from 12% to 23% in major U.S. cities. This high vacancy rate is contributing to the commercial real estate crisis by depressing property values, creating challenges for real estate loans that are coming due.

How might rising office vacancy rates impact the regional banking sector amid the commercial real estate crisis?

High office vacancy rates could lead to significant delinquencies on commercial real estate loans, particularly affecting regional banks that have heavily invested in these properties. If many of these loans default, it could strain the banking sector and impact local economies.

What economic impacts can be anticipated from the ongoing commercial real estate crisis?

The commercial real estate crisis, marked by increased office vacancies, could result in lower consumption, stricter lending terms, and potential bankruptcies among real estate firms. However, the overall economy might not see severe effects, given a strong job market and stock performance.

Are financial regulations adequate to mitigate the risks from the commercial real estate crisis?

After the 2008 financial crisis, stricter financial regulations for large banks were implemented. These regulations may help them withstand the risks posed by the commercial real estate crisis, though smaller regional banks might face greater vulnerabilities due to less stringent oversight.

What role do real estate loans play in the commercial real estate crisis?

Real estate loans, particularly those nearing maturity, are central to the commercial real estate crisis. About 20% of the $4.7 trillion commercial mortgage debt is due this year, and defaults could have cascading effects on bank stability and the broader economy.

How can the economic repercussions of the commercial real estate crisis be mitigated?

Mitigating the economic repercussions of the commercial real estate crisis could involve reducing long-term interest rates to aid in refinancing. However, this is unlikely without a significant economic downturn, and some bankruptcies in the sector are expected as part of the adjustment process.

What could happen if significant delinquencies occur in the commercial real estate loan sector?

If significant delinquencies occur in the commercial real estate loan sector, it could lead to instability in regional banks, reduced lending, and broader economic impacts. However, major banks are better equipped to absorb these losses due to more diversified portfolios.

Is there a risk of widespread bank failures linked to the commercial real estate crisis?

While some banks, particularly regional ones, may face risks due to their exposure to commercial real estate loans, widespread bank failures are not expected. Large banks have greater resilience and a diversified income base, which buffers them against localized crises.

How do high office vacancy rates correlate with commercial real estate property values?

High office vacancy rates are negatively impacting commercial real estate property values, as buildings are selling for significantly less than previous market prices. This depreciation is a key component of the current commercial real estate crisis.

What should investors consider regarding the commercial real estate crisis?

Investors should be cautious about the commercial real estate crisis, particularly in light of high office vacancy rates and the looming maturity of substantial real estate loans. Diversification and an understanding of market dynamics are crucial as the situation evolves.

| Key Points |

|---|

| High office vacancy rates (12% – 23%) are depressing property values and could impact the economy. |

| 20% of $4.7 trillion commercial mortgage debt due this year poses potential risks to banks and investors. |

| Kenneth Rogoff believes not all banks will fail, but some smaller and less regulated ones could face crises. |

| Commercial real estate was over-leveraged due to historically low interest rates before pandemic disruptions. |

| Some segments, like premium buildings, are still performing well, yet overall occupancy is still low. |

| A slow pace of redevelopment from office to residential use complicates the crisis response. |

| High interest rates could continue affecting refinancing and lead to bankruptcies in real estate. |

| Regional banks heavily invested in commercial real estate are vulnerable if delinquencies rise. |

| Major banks are better positioned to withstand potential defaults compared to smaller banks. |

Summary

The commercial real estate crisis presents substantial challenges, particularly due to the high office vacancy rates and looming debt maturities impacting banks and investors. While some institutions could face significant losses, not all are at risk of failure as seen in the past financial crises. The divergent performance within the real estate sector and the banks’ ability to navigate these challenges indicate that while the crisis is serious, the overall economy may not be significantly impacted unless there are further economic shocks.